Impôt sur le revenu - Travaux d'adaptation du logement à la perte d'autonomie liée à l'âge ou au handicap (crédit d'impôt)

Vérifié le 15 avril 2026 - Service Public / Direction de l'information légale et administrative (Premier ministre)

Vous avez fait effectuer dans votre domicile en 2025 des travaux d'équipement pour personne en situation de handicap ou âgée en perte d'autonomie ? Vous pouvez bénéficier, sous conditions, d'un crédit d'impôt pour les travaux réalisés et facturés avant le 31 décembre 2025. Le crédit d’impôt est supprimé pour les dépenses payées à partir du 1er janvier 2026. Nous vous indiquons les informations à connaître pour vos dépenses de 2025.

Dépenses payées en 2025

Le crédit d'impôt est désormais réservé aux personnes ayant des revenus intermédiaires, qui remplissent certaines conditions.

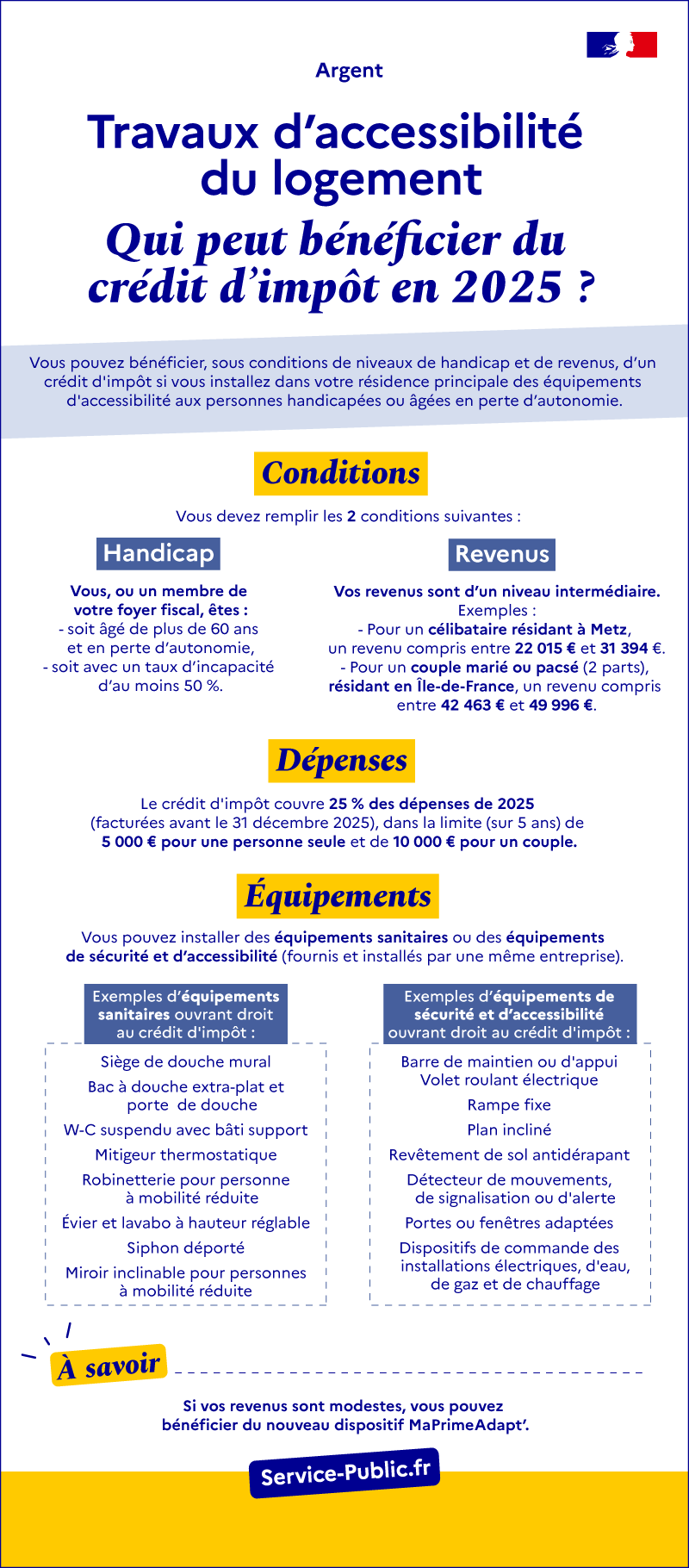

Infographie - Travaux d'accessibilité du logement : qui peut bénéficier du crédit d'impôt ?

Ouvrir l’image dans une nouvelle fenêtre

Titre : Travaux d'accessibilité du logement : qui peut bénéficier du crédit d'impôt en 2025 ?

Vous pouvez bénéficier, sous conditions de niveaux de handicap et de revenus, d’un crédit d'impôt si vous installez dans votre résidence principale des équipements d'accessibilité aux personnes handicapées ou âgées en perte d’autonomie.

Conditions

Vous devez remplir les 2 conditions suivantes :

1/ Handicap

Vous, ou un membre de votre foyer fiscal, êtes soit âgé de plus de 60 ans et en perte d’autonomie, soit avec un taux d’incapacité d’au moins 50 %.

2/ Revenus

Vos revenus sont d’un niveau intermédiaire.

Exemples :

Pour un célibataire résidant à Metz : un revenu compris entre 22 015 € et 31 394 €.

Pour un couple marié résidant en Île-de-France : un revenu compris entre 42 463 € et 49 996 €.

Dépenses

Le crédit d'impôt couvre 25 % des dépenses de 2025 (facturées avant le 31 décembre 2025), dans la limite (sur 5 ans) de 5 000 € pour une personne seule et de 10 000 € pour un couple.

Équipements

Vous pouvez installer des équipements sanitaires ou des équipements de sécurité et d’accessibilité (fournis et installés par une même entreprise).

Exemples d’équipements sanitaires ouvrant droit au crédit d'impôt :

- Siège de douche mural

- Bac à douche extra-plat et porte de douche

- W-C suspendu avec bâti support

- Mitigeur thermostatique

- Robinetterie pour personne à mobilité réduite

- Évier et lavabo à hauteur réglable

- Siphon déporté

- Miroir inclinable pour personnes à mobilité réduite

Exemples d’équipements de sécurité et d’accessibilité ouvrant droit au crédit d'impôt :

- Barre de maintien ou d'appui

- Volet roulant électrique

- Rampe fixe

- Plan incliné

- Revêtement de sol antidérapant

- Détecteur de mouvements, de signalisation ou d'alerte

- Portes ou fenêtres adaptées

- Dispositifs de commande des installations électriques, d'eau, de gaz et de chauffage

À savoir : Si vos revenus sont modestes, vous pouvez bénéficier du nouveau dispositif MaPrimeAdapt’.

Logement

Vous devez être domicilié fiscalement en France et ce logement doit être votre habitation principale.

Vous pouvez être propriétaire, locataire ou occupant à titre gratuit du logement.

Vous devez faire effectuer des travaux dans votre logement.

Si vous êtes locataire, vous devez demander l'autorisation préalable de votre bailleur.

Si vous habitez dans un immeuble collectif, dans lequel des travaux ont été effectués sur les équipements communs, vous bénéficiez du crédit d'impôt pour votre part des dépenses.

Attention

Les travaux doivent être effectués par la même entreprise.

Personnes concernées

Le crédit d'impôt est placé sous conditions de ressources.

Il est réservé aux personnes ayant des revenus intermédiaires.

À savoir

Si vos revenus sont modestes ou très modestes, vous pouvez demander à bénéficier du dispositif MaPrimeAdapt'. Vous ne pouvez pas bénéficier à la fois du crédit d'impôt et de la prime.

Pour bénéficier du crédit d'impôt, vous, ou un membre de votre foyer fiscal: titleContent, devez être dans l'une des situations suivantes :

- Âgé de 60 ans ou plus et avec une perte d'autonomie qui vous classe dans l'un des groupes 1 à 4 de la grille nationale applicable pour l'allocation personnalisée d'autonomie

- Avec un taux d'incapacité supérieur ou égal à 50 % (taux déterminé par décision de la CDAPH: titleContent).

Vous devez aussi remplir des conditions de revenus.

Les revenus annuels de votre ménage doivent être supérieurs aux revenus suivants :

Nombre de personnes composant le ménage | Revenus Île-de-France | Revenus autres régions |

|---|---|---|

1 | 28 933 € | 22 015 € |

2 | 42 463 € | 32 197 € |

3 | 51 000 € | 38 719 € |

4 | 59 549 € | 45 234 € |

5 | 68 123 € | 51 775 € |

Par personne supplémentaire | 8 568 € | 6 525 € |

À noter

Si vos revenus de 2023 sont inférieurs ou égaux à ces seuils, on retient vos revenus de 2024.

Vos revenus annuels doivent aussi être inférieurs à des plafonds calculés en fonction du nombre de parts de votre foyer fiscal: titleContent.

Les plafonds de revenus sont calculés selon les montants suivants :

- 31 394 € pour la 1re part de quotient familial

- 9 301 € pour chacune des 2 demi-parts suivantes

- 6 976 € pour chaque demi-part supplémentaire à compter de la 3e.

À noter

Si vos revenus de 2023 sont supérieurs ou égaux à ces plafonds, on retient vos revenus de 2024.

Exemple :

Pour un couple marié ou pacsé (2 parts) résidant en Île-de-France.

Le revenu minimum pour bénéficier du crédit d'impôt est de 42 463 €.

Le revenu à ne pas dépasser pour pouvoir en bénéficier est de : 31 394 € + (9 301 € x 2) = 49 996 €.

Les revenus annuels du couple doivent être compris entre 42 463 € et 49 996 €.

Exemple :

Pour une personne célibataire (1 part) résidant à Metz.

Le revenu minimum pour bénéficier du crédit d'impôt est de 22 015 €.

Le revenu à ne pas dépasser pour pouvoir en bénéficier est de 31 394 €.

Les revenus de la personne célibataire doivent être compris entre 22 015 € et 31 394 €.

Date des travaux

Les travaux doivent être réalisés et facturés avant le 31 décembre 2025.

Le versement d’un acompte: titleContent, notamment lors de l’acceptation du devis, n'est pas considéré comme un paiement pour le crédit d’impôt.

Le paiement est considéré comme intervenu lors du règlement définitif de la facture.

Exemple :

Vous avez payé un acompte en 2024.

La facture a été émise en décembre 2024 et vous avez réglé le solde en janvier 2025.

Le crédit d’impôt est ouvert pour l'imposition de vos revenus de 2025 (déclaration en 2026), pour l’ensemble de la dépense supportée.

Si vous êtes en copropriété et que les travaux sont payés par l'intermédiaire du syndic, la date prise en compte est celle du paiement du montant des travaux à l’entreprise qui les a effectués.

Ce n'est pas la date du versement de vos appels de fonds.

Vous devez faire effectuer dans votre logement des travaux d'adaptation du logement à la perte d'autonomie ou au handicap.

Les travaux d'installation et de remplacement des équipements sont concernés.

Vous devez avoir fait installer dans votre logement un ou plusieurs équipements des catégories suivantes :

- Équipements sanitaires

- Équipements de sécurité et d'accessibilité.

Les équipements concernés sont les suivants :

Répondez aux questions successives et les réponses s’afficheront automatiquement

Équipements sanitaires

- Évier et lavabo à hauteur réglable

- Évier et lavabo fixe utilisable par une personne à mobilité réduite

- Siphon déporté

- Siège de douche mural

- Cabine de douche intégrale pour personne à mobilité réduite

- Bac à douche extra-plat et porte de douche

- Receveur de douche à carreler

- Pompe de relevage ou pompe d'aspiration des eaux pour receveur extra-plat

- W-C surélevé

- W-C suspendu avec bâti support

- W-C équipé d'un système lavant et séchant

- Robinetterie pour personne à mobilité réduite

- Mitigeur thermostatique

- Miroir inclinable pour personnes à mobilité réduite.

Équipements de sécurité et d'accessibilité

- Barre de maintien ou d'appui

- Main courante

- Système de motorisation de volets, de portes d'entrée et de garage, de portail

- Volet roulant électrique

- Système de commande comprenant un détecteur de mouvements, de signalisation ou d'alerte

- Dispositif de fermeture, d'ouverture ou système de commande des installations électriques, d'eau, de gaz et de chauffage

- Éclairage temporisé couplé à un détecteur de mouvements

- Poignée ou barre de tirage de porte adaptée

- Système de transfert à demeure ou potence au plafond

- Rampe fixe

- Plan incliné

- Mobilier à hauteur réglable

- Revêtement podotactile

- Nez de marche contrasté et antidérapant

- Revêtement de sol antidérapant

- Protection d'angles

- Garde-corps

- Porte ou fenêtre adaptée

- Inversion ou élargissement de porte

- Porte coulissante

- Boucle magnétique

- Appareil élévateur vertical comportant une plate-forme aménagée en vue du transport d'une personne handicapée et élévateur à déplacement incliné spécialement conçu pour le déplacement d'une personne handicapée.

Dépenses concernées

Les dépenses prises en compte pour le crédit d'impôt sont les suivantes :

- Prix d’achat des équipements (ou matériaux)

- Frais de main-d'œuvre.

Les frais administratifs ou financiers (intérêts par exemple) sont exclus.

Ce sont uniquement les dépenses que vous avez effectivement payées.

Si vous avez touché une aide financière, vous devez donc la déduire.

Taux du crédit d'impôt

Le taux est de 25 % du montant des dépenses.

Plafond de dépenses

Les dépenses sont plafonnées à l'un des montants suivants :

- 5 000 € pour une personne seule

- 10 000 € pour un couple marié ou pacsé soumis à imposition commune.

Ce plafond est majoré de 400 € par personne à charge (200 € par enfant en résidence alternée).

Attention

Ce plafond est fixé pour une période de 5 années consécutives. Par exemple, pour l'année 2025, il concerne les dépenses entre le 1er janvier 2021 au 31 décembre 2025.

Vous devrez déclarer en 2025 vos dépenses payées en 2024.

Conservez vos justificatifs de dépenses car l'administration fiscale peut vous les demander (facture de l'entreprise, attestation du vendeur).

Si le montant du crédit d'impôt dépasse celui de l'impôt dû, l'excédent vous sera restitué.

Dépenses payées en 2026

Vous ne pouvez pas bénéficier du crédit d’impôt pour vos dépenses payées en 2026.

À savoir

Si vos revenus sont modestes ou très modestes, vous pouvez demander à bénéficier du dispositif MaPrimeAdapt'.

Qui peut m'aider ?

Vous avez une question ? Vous souhaitez être accompagné(e) dans vos démarches ?

Pour des informations générales

Par téléphone :

0809 401 401

Du lundi au vendredi de 8h30 à 19h, hors jours fériés.

Service gratuit + prix appel

Pour joindre le service local gestionnaire de votre dossier

Service en charge des impôts (trésorerie, service des impôts...)

Crédit d'impôt pour dépenses en faveur de l'aide aux personnes (article 200 quater A)

Liste des équipements spécialement conçus pour les personnes âgées ou handicapées (article 18 ter)

Service en ligne

Service en ligne

Questions ? Réponses !

Service Public

Service Public

Ministère chargé des finances

Ministère chargé des finances

Ministère chargé des finances

Ministère chargé des finances

Agence nationale de l'habitat (Anah)

Cette page vous a-t-elle été utile ?

Cette page vous a-t-elle été utile ?

- 1

- 2

- 3

- 4

- 5

Pas du tout

Un peu

Moyen

Beaucoup

Parfait !

L’équipe Service Public vous remercie

L’équipe Service Public vous remercie pour vos remarques utiles à l'amélioration du site.

Pour des raisons de sécurité, nous ne pouvons valider ce formulaire suite à une trop longue période d’inactivité. Merci de recharger la page si vous souhaitez le soumettre à nouveau.

Une erreur technique s'est produite. Merci de réessayer ultérieurement.